Pro-AV Business Index

April: Increasing costs slow Demand

Highlights

The AV Sales Index (AVI-S) for April dropped 7 points to 52.2, with 21% of respondents saying they saw a decrease in sales for the month. This most likely means buyers are still active but are moderating spend, leading to softer revenue outcomes despite continued deployment activity. Companies are saying they have a good pipeline through 2026.

Tariff uncertainty, geopolitical conflict, and economic instability are the dominant concerns, making it difficult to forecast, price projects, and close sales. However, seasonal patterns in education and a few other vertical markets provide optimism for the coming months.

The March AV Employment Index (AVI-E) remained steady at 54.2 in April. The U.S. job growth rebounded but at a slower pace than last year’s norms. Some are finding it hard to hire skilled employees while others are freezing hiring.

International Outlook

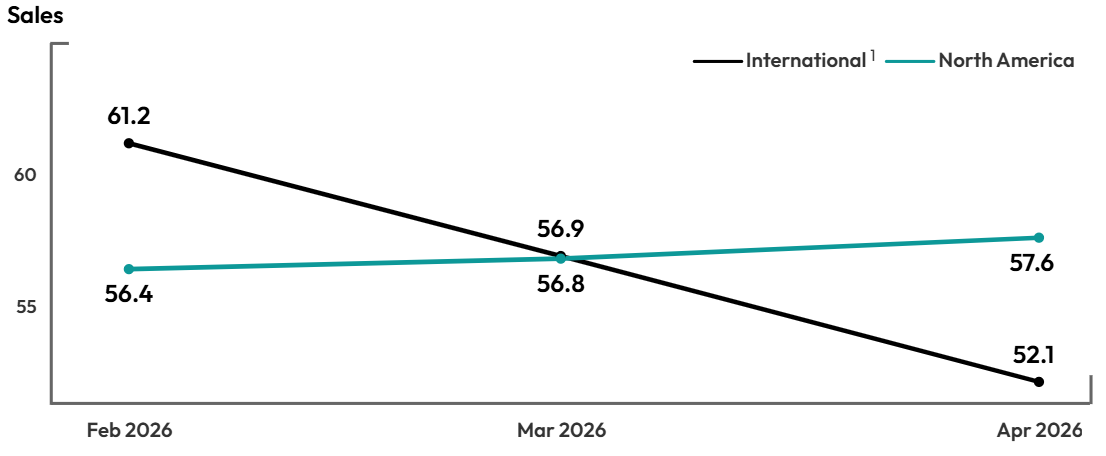

The preliminary North American AV Sales Index (AVI S) rose one point to 57.6 in April, while the non North America sales index dropped to 52.1. While global supply chains stabilize, regional friction remains such as logistics complexity in Southeast Asia, Eastern Europe and Middle East. On the employment side, the North American AVI E increased to 56.7 while the non North America AVI E remained steady showing no expansion or decrease at 50.1 for April. Labor dynamics diverged sharply by region. North America continued modest employment expansion, reflecting flexible labor practices and selective hiring. In contrast, employment across EMEA and APAC remained flat, driven by seasonal pauses, public sector budget timing, and more risk averse hiring structures. These patterns point to deferred execution rather than deteriorating demand in international markets.

1Due to the small sample, the North American and International indexes are based on a 3-month moving average. The April 2026 index is preliminary, based on the average of April 2026 and March 2026 and will be final with May 2026 data in the next report.

1AVIXA®, the Audiovisual and Integrated Experience Association, has published the monthly Pro AV Business Index since September 2016, gauging sales and employment indicators for the pro AV industry. The index is calculated from a monthly survey that tracks trends. Two diffusion indexes are created using the survey: the AV Sales Index (AVI-S) and AV Employment Index (AVI-E). The diffusion indexes are calculated based on the positive response frequency from those who indicated their business had a 5% or more increase in billings/sales from the prior month plus half of the neutral response. An index of 50 indicates firms saw no increase or decline in business activity; more than 50 indicates an increase, while less than 50 indicates a decrease.

I feel the political scene and the unrest in Iran is causing apprehension and disruption in the market. Yet, we remain busy, especially with higher education installation season upon us

Distributor, North America

Constantly changing tariff add-ons make it difficult to provide clients with accurate cost assessment for projects. In addition, frustration with paying tariffs to vendors knowing they'll be the ones to collect any refunds instead of giving them back makes one question the legality of vendors even being allowed to charge them to us in the first place

End User, North America

Our business is currently driven by the rapid integration of AI automated environment and a high demand for sustainable

AV Integrator, North America

Methodology

The survey behind the AVIXA Pro AV Business Index was fielded to 2,000 members of the AVIXA Insights Community between March 26, 2026 and April 6 2026. A total of 269 AV professionals completed the survey. Only respondents who are service providers and said they were “moderately” to “extremely” familiar with their company’s business conditions were factored in index calculations. The AV Sales and AV Employment Indexes are computed as diffusion indexes. The monthly score is calculated as the percentage of firms reporting a significant increase plus half the percentage of firms reporting no change. Comparisons are always made to the previous month. Diffusion indexes, typically centered at a score of 50, are used frequently to measure change in economic activity. If an equal share of firms reports an increase as reports a decrease, the score for that month will be 50. A score higher than 50 indicates that firms, in the aggregate, are reporting an increase in activity that month compared to the previous month. In contrast, a score lower than 50 is a decrease in activity.

About the AVIXA Insights Community

The AVIXA AV Intelligence Panel (AVIP) is now part of AVIXA’s Insights Community, a research group of industry volunteers willing to share their insights on a regular basis to create actionable information. Members of the community are asked to participate in a short, two-to-three-minute monthly survey designed to gauge business sentiment and trends in the AV industry. Community members will also have the opportunity to participate in discussions, polls and surveys.

Community members will be eligible to:

- Earn points toward online gift cards

- Receive free copies of selected market research

- Engage directly with AVIXA's market intelligence team to help guide research

- Ask and answer other industry professionals' questions

The Insights Community is designed to be a global group, representative of the entire commercial AV value chain. AVIXA invites AV integrators, consultants, manufacturers, distributors, resellers, live events professionals, and AV technology managers to get involved. If you would like to join the community, enjoy benefits, and share your insights with the AV industry, please apply here